Key actions CFOs must take to drive profitable growth and improve returns from digital spending.

- Gartner client? Log in for personalized search results.

Driving Business Growth — Key Insights for Finance Leaders

Emerge stronger by making 2023 the year of efficiency

A small number of companies broke away from the pack during the Great Recession and sustained their performance for the subsequent decade. As the threat of another downturn looms, CFOs should revisit lessons from the past — in particular, that outperformers win because of the decisive actions they take.

Download this eBook for ideas to:

- Manage spend in a way that preserves investments for strategic initiatives

- Secure talent at a discount by rethinking how the organization leverages human capital

- Accelerate digital based on a future vision of the organization and its customer

5 actions finance leaders can take to drive business growth

High interest rates, scarce and expensive talent, and lagging digital transformation are all keeping organizations from driving business growth and profitability. CFOs looking for the best opportunities will focus on the following core activities.

- Boost Digital Cohesion

- Make Big Growth Bets

- Drive COGS Efficiency Over SG&A

- Spend for Cost Differentiation

- Embrace Capital Activism

Increase the returns from digital investments by leveraging interdependencies

A Gartner survey of CFOs finds that around 80% plan to maintain or increase digital investment levels in 2023. Despite continued spending and continued expectations that digital investments drive business growth, only 33% of CFOs report that digital spending has met or exceeded expectations. Revenue attributed to digital is on average between zero and 5% of total enterprise revenues, for instance, and productivity has flatlined since 2015.

Those are averages, however. Some organizations are meeting or exceeding expectations from digital spending. Those that do outperform those that don’t by 2.8x. These superior returns are the combined result of two key actions: digital discipline and digital cohesion.

Digital discipline delivers about 41% of the value realized by the organizations that meet or exceed digital expectations. It requires finance to:

Vet business cases for digital spending

Collaboratively define KPIs for new digital projects

Hold business leaders accountable for digital outcomes

Digital discipline is difficult to achieve, however, due to the fact that finance leaders typically lack familiarity with digital business cases and don’t know what the right KPIs should be at the outset of a new initiative. Moreover, digital investments are often cross-functional, requiring input from multiple business units — holding one business leader accountable for outcomes overlooks the diffuse responsibilities and diffuse benefits that digital capabilities enable.

Fully benefiting from digital investments requires not just digital discipline but digital cohesion to improve enterprise-level outcomes. Digital cohesion requires that finance:

Understand key interdependencies between digital initiatives

Create an enterprise digital “roadmap” that identifies challenges, conflicts and gaps in connecting digital initiatives to enterprise outcomes

Update “roadmap” assumptions based on new insights

Evolve the operating model to support interconnectivity between digital initiatives

Establish cross-functional teams to manage interdependencies

Adopt the growth practices of efficient growth companies

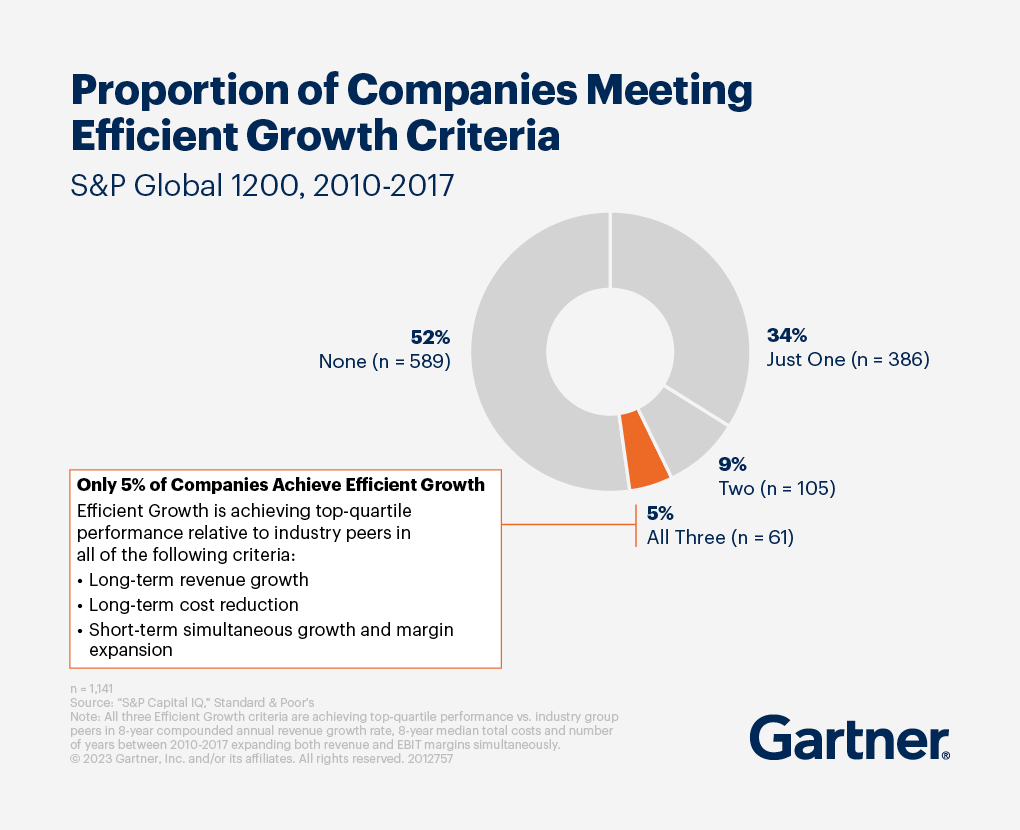

Efficient growth leaders — defined by Gartner analysis of more than 1,000 S&P Global 1200 companies — have sustained long-term revenue growth with simultaneous margin improvements over the past 20 years. They see a 7.1% return premium over their peers. These companies are rare. Since 2010, only 5% of S&P Global 1200 organizations fall into this category. The ones that do embrace the following growth practices:

Instill cycle discipline. Plan around all four phases of the business cycle: stable growth, peak, recession and trough. This means that organizations still seek to reduce operating costs when economic growth is strong and invest in opportunities when it’s weak.

Remove growth anchors; preserve growth ladders. Make bigger, riskier growth bets to deliver outsized growth over the long term. Examples include pursuing larger M&A deals as a percentage of revenue, prioritizing R&D spending on transformational innovation and reintroducing capital expenditures faster after a recession than their control peers.

At the same time, finance must remove “growth anchors,” which cause business managers to redirect resources away from growth projects — such as lengthier evaluation processes for higher-risk projects, resulting in delayed project funding.

Cultivate overperformance instead of correcting underperformance. Finance teams tend to focus on minimizing the number of investments that miss their initial expectations rather than maximizing their total returns. As a result, they spend a disproportionate amount of time and resources vetting business cases, holding business leaders accountable and course-correcting underperforming investments. These actions don’t produce the desired results.

Instead, the most successful finance teams adjust the planned level of funding so they can pull back on underperforming investments and add funds to higher-potential opportunities. They also minimize resource interdependencies between projects. As a result, these companies achieve the desired internal rate of return (IRR) on their overall investment portfolio.

Focus on scale, not scope. Most companies inadvertently add scope as they pursue growth. This creates complexity that inflates cost structures and weakens competitiveness. Efficient growth companies, in contrast, compete in fewer industries, book more revenue in their largest geographic segment and consolidate their products and services into fewer lines of business than their peers. As a result, they achieve 10-percentage-point higher operating cost productivity, as well as cost reduction periods that last for almost 40% longer.

Pursue cost differentiation. Adapting the cost structure to extrinsic factors based on the growth plans of the CEO and business unit executives — all driven by the opportunities and dynamics in their markets — has been touted as a key CFO leadership practice. But Gartner analysis found that adaptiveness has zero impact on a company’s ability to realize long-term value. Differentiating the cost structure based on intrinsic factors, in contrast, produces an average return premium of six percentage points.

Managing COGS more than SG&A delivers cost advantages for profitability

The competitive pressure to drive top-line business growth has caused costs to outpace revenue. CFOs are urgently seeking ways to translate long-term growth bets into sustained profitability. Beyond adopting growth practices, efficient growth companies achieve profitable growth by focusing on scale in the cost structure instead of on scope.

That focus on scale shows up in the following activities in efficiency growth companies compared to similar-size competitors. They:

Invest in 18% fewer industries in their business portfolios and pursue adjacent expansion only when they can leverage fixed costs

Structure product and service lines into 24% fewer segments, focusing overhead investment on a simpler product and service mix

Concentrate customer acquisition and operational footprint, deriving 20% more revenue from their largest geographic segments

Overall, these activities deliver faster earnings growth relative to revenue.

Embracing these practices can present a complex challenge, however. This is especially true for organizations pursuing a business growth strategy through M&A, entering new markets and developing new products, all of which require investment in operating costs. For example, when organizations diversify into adjacent industries, CFOs are forced to spread fixed costs across a wider array of product and service lines and geographic segments. This decreases the leverage companies can achieve from functional and operating costs.

Efficient growth companies combat that challenge through scale-focused investments to achieve 10.9-percentage-point higher operating cost productivity (a measure of how much earnings growth outpaced revenue growth). They also sustain productive cost-saving periods for longer than their peers.

Although selling, general and administrative (SG&A) and cost of goods sold (COGS) are the dominant operating costs on income statements, their impact on performance is not equal. Efficient growth companies derive a 9% COGS-over-revenue cost advantage over peer companies, but their performance on SG&A cost management is not statistically different from their nongrowth peers. The degree of advantage differs by industry, but COGS dominates the operating cost base of all industries except financial services.

Unlock differentiation through your cost structure

Cost differentiation involves spending to support capabilities that competitors cannot replicate. Gartner research on spending for growth shows that taking a cost differentiation approach can result in a 42% increase in long-term value, which translates to six percentage points of excess returns compared to peers.

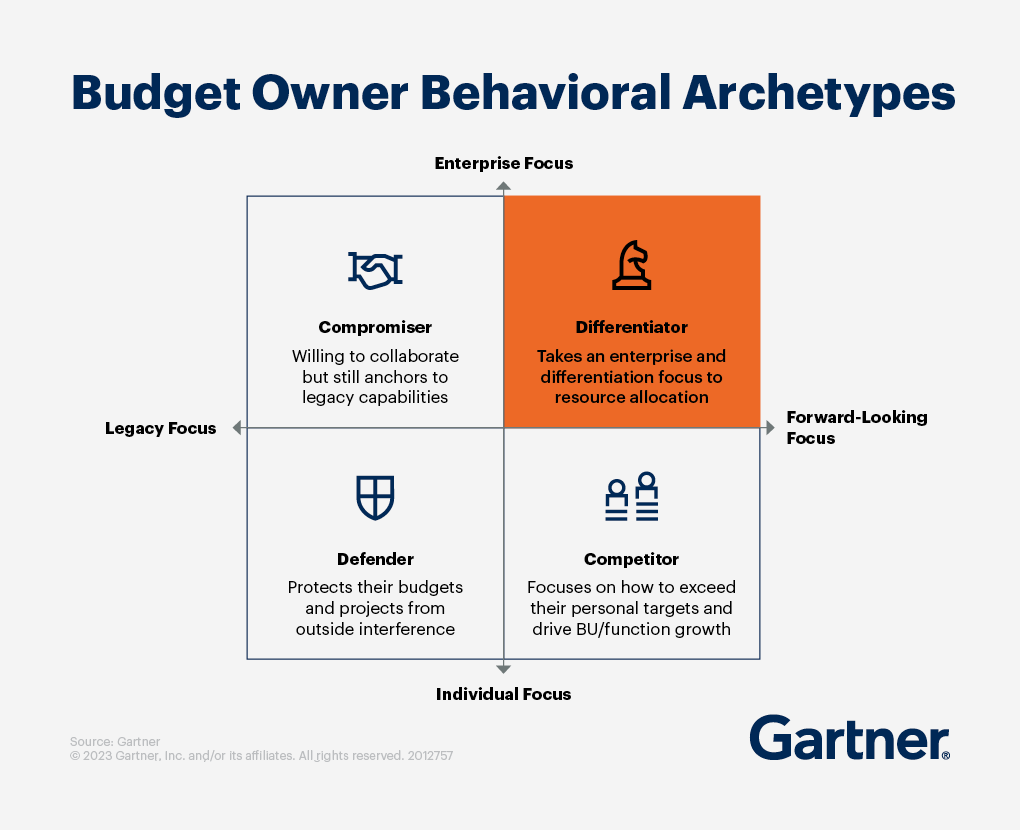

CFOs cannot achieve cost differentiation on their own. It requires cooperation from budget owners. Unfortunately, common attitudes and behaviors by business leaders work against differentiation. For example, viewing their budget in isolation and holding fast to legacy capabilities or products prevent cost differentiation.

CFOs can take steps to change budget owner attitudes and behaviors by understanding the three budget owner archetypes and adopting interventions for those who resist a differentiated spend strategy. Consider the following archetypes and interventions:

The Defender is individually focused and anchored to their legacy costs and as a result is most territorial and resistant to spending changes. Creating clear rewards for moving away from legacy costs can motivate Defenders to make resource allocation choices that support differentiation. For example, CFOs can incentivize Defenders by implementing a win-back process, which rewards cuts in nondifferentiating legacy costs with funds to invest in differentiating costs.

To ensure the result of any win-back program contributes to cost differentiation, finance must establish guardrails by working with budget owners to create a list of resource allocation decisions that would support differentiation and long-term value creation.

The Competitor focuses on advancing their own priorities and goals with a zero-sum attitude that manifests in competition over scarce resources. The Competitor is enabled by siloed processes and incentives that treat business unit budgets and performance as more important than those of the enterprise as a whole.

Adopting an enterprisewide and collaborative approach to budget processes can help Competitors see how costs cut across budgets. During group sessions, budget owners have to justify how their costs create long-term value for the organization. Competitors who advocate for resource allocation that only promotes their priorities will face challenges from their peers.

Organizations may also need to rebalance performance incentives away from individual-level targets and toward corporate-level performance. While the precise mix will vary by organization, more heavily weighting incentives toward enterprisewide performance will eliminate some resistance to cost differentiation.

The Compromiser willingly participates in enterprisewide budget decisions but tends to anchor to existing cost structures and has an attachment to legacy costs and capabilities they see as important for success.

CFOs can remove attachments to legacy costs by reminding budget owners which differentiating capabilities the organization is promoting and how the Compromiser’s team contributes to them. To do so, build a business capability model that lists the capabilities that create value for customers and highlight the differentiating ones. Complement that model with capability ownership maps that show which teams are responsible for differentiating capabilities and how they drive growth and profitability. Further connect these insights to capability-based funding models to help budget owners make resource allocation decisions.

Become an internal capital activist

In today’s disruptive economic environment, sound planning is no longer enough to ensure optimal use of organizational capital to drive growth. Instead, CFOs need to embrace capital responsiveness, or the ability to respond to changing business conditions, in the following ways:

Quickly shift capital to new high-value uses.

Quickly shift capital away from new low-value uses.

Make significant, rather than incremental, changes to where capital is allocated.

Relatively few companies achieve any one of these, and only 17% can do all three, which is necessary to maximize enterprise returns. Those that do earn an average of 2.5 percentage points more in economic value added (return on invested capital — weighted average cost of capital) than “unresponsive” peers.

Transforming into a responsive firm requires finance leaders to become capital activists — that is, to apply the approaches of the most productive activist investors and private equity firms to the organization. Capital activists improve a company’s capital responsiveness by challenging the business attachments to legacy investments and siloed value creation.

Capital activism moves beyond the “reviewer” or “advisor” role most finance leaders play. It may still be appropriate for finance leaders, in certain contexts, to pressure-test the assumptions underlying business investments and their alignment with enterprise goals (e.g., reviewer activities) and to help guide business leaders toward strategic priorities, balance funding allocation across those priorities and analyze metrics related to initiative performance (e.g., advisor activities). But activist CFOs will overall play a more active role in determining where to invest, how to distribute funding and how to ensure successful execution.

Capital activism does not call for finance to take investment decisions away from the business units. It does, however, require that finance influence decisions by guiding leaders to focus on long-term, enterprisewide value creation, rather than short-term and/or siloed priorities.

Gartner CFO & Finance Executive Conference

Be a part of most important gathering for CFOs to explore potential finance tech providers and get actionable insights to prioritize technology innovation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Gartner delivers actionable, objective insight to executives and their teams.

What is holding back business growth in today’s market?

Inflation, the high costs and limited supply of talent and materials, and low returns on digital investment are all contributing to drag down growth in 2023.

How can finance leaders increase returns from digital investments?

Businesses that achieve outside returns from digital investments adopt two practices: digital discipline and digital cohesion. Digital discipline requires that finance leaders vet business cases for digital spending, collaboratively define digital KPIs with business leaders and hold business leaders accountable for promised digital outcomes. Digital cohesion, in turn, requires that finance leaders understand key interdependencies between digital initiatives to identify opportunities, as well as challenges, conflicts and gaps in connecting them to enterprise outcomes, and evolve their operating models and team structures to support interconnectivity between digital initiatives.

What actions can finance leaders take to drive business growth?

Finance leaders can set the stage for their organizations to grow in 2023 by taking steps to increase returns from digital investments, establishing practices that allow fast allocation of funds into high-potential initiatives and away from low performers, managing COGS more than SG&A and embracing cost differentiation.

What is capital responsiveness in finance?

Capital responsiveness is the ability to respond to changing business conditions by quickly shifting capital to new high-value uses and away from low-value uses and making significant (rather than incremental) changes to where capital is allocated.